A Guide to Family Business and Succession Planning

Business owners nearing retirement or preparing to step back from their business often face two connected questions: what to pass on and the best way to pass it on through family business and succession planning. A succession strong plan helps turn values into formal documentation, leadership into continuity, and years of work into a transition plan that supports your goals. Handled with care, family business and succession planning becomes a process that protects your financial positioning, relationships, and the business you’ve built.

Why It Pays to Start Family Business and Succession Planning Early

When decisions are delayed, valuation work, tax modeling, and successor development can get squeezed into a high-pressure rush. Starting sooner gives you breathing room to evaluate paths, set expectations clearly, and adjust as life circumstances or market realities shift.

Signs You May Be Ready to Start Planning

- You expect to scale back your day-to-day role within the next five years.

- No clear successor has emerged, or interest among family members is uneven.

- You’re unsure how to balance liquidity needs with legacy goals and business stability.

- You anticipate regulatory or tax changes that could affect transfer design.

An early start also supports foundational work, including securing an independent valuation, updating governing documents, and identifying liquidity sources for buyouts or taxes. Because the IRS adjusts estate and gift thresholds annually, syncing your timeline and plans to those updates can be useful during family business and succession planning.

If you want an initial readiness check, contact the office to review your priorities, timeline, and documents with your financial professional.

Family Business and Succession Planning Begins With Defining the Outcome You Want

Before selecting legal structures or making any agreements, clarify what a successful transition looks like for you. Clear goals tend to prevent future friction and make technical decisions easier to navigate.

Specifics Worth Putting in Writing

As you begin defining what success might look like, certain details can get overlooked. Here are some details you should consider and discuss with your advisory team and trusted team members.

- Your post-exit role

- Voting control and board or family council parameters

- Liquidity needs for retirement and charitable intentions

- A principle for fairness among heirs who work inside versus outside the business

Once your intentions are documented, your family business and succession planning can connect tax strategy, ownership structure, and governance to those priorities. This is also a good time to establish a communication plan that defines what gets shared, with whom, and when, so fewer decisions come as surprises to stakeholders.

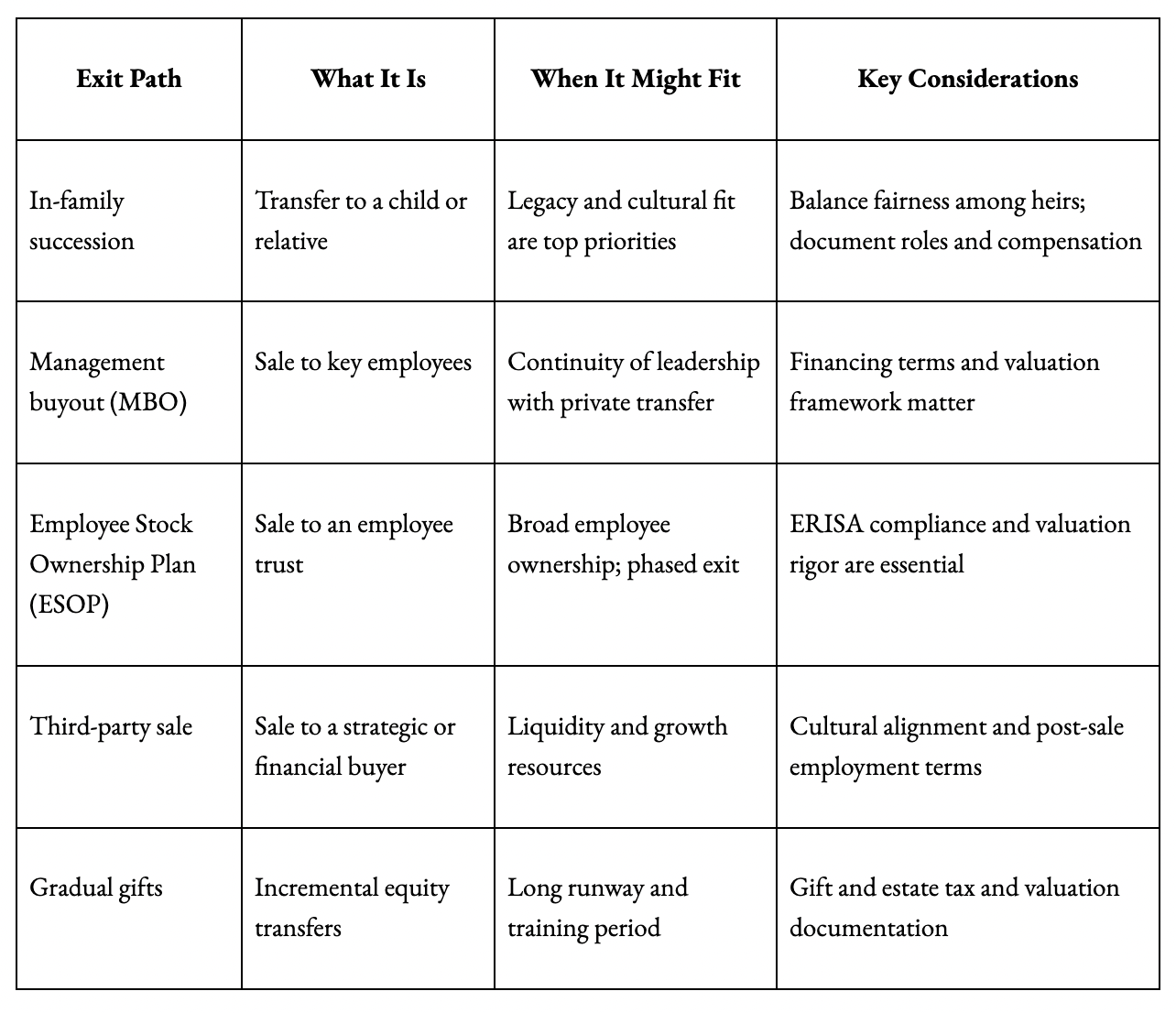

Comparing Common Approaches: Sale, Gift, and Ownership Strategies for Family Business and Succession Planning

These are typical paths owners consider when shaping a family business and succession planning strategy. Each option comes with potential advantages and drawbacks tied to control, cash flow, administration, and cultural continuity.

If your goals for family business and succession planning point toward a sale instead of an in-family transition, the Small Business Administration outlines practical preparation steps, from organizing records to bringing in professional support.

How Valuation and Liquidity Impact Family Business and Succession Planning

Many owners find the most resilient plans are the ones that tie estate documents, buy-sell mechanics, and funding sources into a single, coordinated picture.

Areas to Evaluate Carefully

- Estate and gift thresholds (if gifting plays a role in your plan): The IRS publishes inflation-adjusted amounts and maintains guidance on how pre-sunset gifts interact with future exclusion levels. Coordinate timing and documentation as part of your family business and succession planning.

- Buy-sell agreement terms: Clarify pricing, triggers such as retirement, disability, or death, funding through insurance, cash, or notes, and dispute resolution.

- Independent valuation: Fairness among heirs and compliance both rely on defensible appraisals and contemporaneous records.

- Liquidity mapping: Identify how taxes, buyouts, and retirement income may be funded without overburdening successors or operations.

- Governing documents: Ensure the operating agreement, shareholder agreement, and estate plan reflect your current intent.

If your key planning documents are more than a few years old, contact the office to coordinate updates with an experienced professional.

Roles, Trust, and Handoffs in Family Business and Succession Planning

Transitions tend to work better when roles are well-defined, decision rights are explicit, and communication stays consistent. The relational side of family business and succession planning deserves the same structure and attention as financial and tax preparations.

Governance Practices That Often Support Smoother Transitions:

- Set a cadence for board or family council and management meetings, with written agendas and minutes.

- Define responsibilities, compensation, and evaluation for both outgoing owners and successors.

- Establish conflict-resolution pathways and voting thresholds for major decisions.

- Pair authority with mentoring by sharing customers, vendors, and institutional knowledge in planned steps.

A neutral facilitator, such as your financial professional, can help facilitate difficult conversations and keep discussions productive.

A 24-Month Timeline to Strengthen Family Business and Succession Planning

This pacing can be adjusted based on your situation and guidance from your legal, financial, and tax teams. The goal is to move in deliberate stages that build clarity and readiness over time.

Months 1–6

- Build a planning team, including your financial professional, attorney, CPA, and valuation firm.

- Set goals and non-negotiables, and create or update your communication plan.

- Determine or solidify your succession pathway.

- Commission a valuation and review an existing buy-sell agreement or draft a new one.

Months 7–12

- Prioritize role transitions and mentoring.

- Model liquidity for tax and buyout scenarios and explore ESOP or MBO feasibility if relevant.

- Have your advisory team perform due diligence if considering an MBO

- Align estate documents with ownership intent and funding sources.

Months 13–24

- Execute transfers such as gifts, sales, or trust funding with formal records.

- Pressure-test governance structures in real meetings

- Refine compensation and key performance indicators (KPIs).

- Complete final tax and legal reviews and document successor authority for banks, vendors, and key clients.

Ongoing

- Revisit the plan every one to three years or after major life or tax changes. IRS updates and Department of Labor guidance can affect assumptions, especially for ESOPs and gifting strategies within family business and succession planning.

If you’d like a personalized timeline aligned to your plans and goals, contact the office to schedule a meeting with your financial professional.

Frequently Asked Questions About Family Business and Succession Planning

When should I begin formal family business and succession planning?

It’s generally best to start family business and succession planning five to ten years before retirement. Early preparation provides time to shape tax, valuation, and leadership strategies without pressure.

What if no one in my family wants to take over the business?

Even if no relative is ready or interested, family business and succession planning can include alternatives such as a sale, merger, or management buyout. With proper planning, these options can also preserve business value and honor legacy.

How do I know what my business is really worth during family business and succession planning?

An independent, credentialed valuation establishes fair market value for gifting, selling, or estate purposes. Periodic updates keep figures current and defensible with tax authorities.

Can multiple successors share ownership within a family business and succession planning?

Yes, but shared ownership should come with documented governance, defined voting rights, and conflict-resolution mechanisms. Written clarity helps prevent confusion after ownership transfers.

How often should I update my family business and succession planning documents?

Every one to three years, or after major shifts in health, tax law, or business structure. Frequent reviews keep the plan relevant to both family dynamics and market changes.

How do taxes affect family business and succession planning?

Federal and state estate and gift tax thresholds influence timing and structure. Early collaboration among financial, tax, and legal professionals helps align goals with compliance.

What are the advantages of keeping the business in the family through family business and succession planning?

Continuity of culture, brand reputation, and community relationships often motivate in-family transfers. However, successors should still meet objective leadership and financial criteria.

What if my heirs disagree about leadership or fairness during family business and succession planning?

A neutral facilitator can help guide structured conversations. Formal governance frameworks and clear valuation methods reduce potential resentment or misunderstanding.

Are employee ownership options like ESOPs practical as part of family business and succession planning?

Sometimes. ESOPs can create liquidity and reward employees while maintaining continuity, but they require regulatory compliance and professional administration.

What role does insurance play in family business and succession planning?

Insurance, such as life or disability coverage, often funds buy-sell agreements or provides liquidity for estate taxes. Reviewing coverage alongside your plan can prevent future financial strain.

How can a financial professional help my family with family business and succession planning?

A financial professional coordinates legal, tax, and interpersonal factors. Their guidance keeps timelines realistic and decisions grounded in objective data rather than emotion.

How long does family business and succession planning usually take?

Most transitions unfold over 18 to 36 months. The pace depends on business complexity, financing, and how ready successors are to assume leadership roles.

What happens if I pass away before completing my family business and succession planning process?

Having interim documents, like buy-sell agreements and estate plans, ensures continuity. Up-to-date paperwork prevents emergency decision-making and supports your family’s stability.

What are the most common mistakes to avoid in family business and succession planning?

- Waiting too long to start

- Relying on verbal promises instead of written plans

- Overlooking tax or legal details

- Neglecting successor training or liquidity needs

Addressing these early can help create clarity and reduce future conflict.

Is family business and succession planning only necessary for large companies?

No. Businesses of every size benefit from structured preparation. Even modest enterprises can protect income, jobs, and legacy through thoughtful family business and succession planning.

Strengthening Your Transition Plan with a Clear Process

A successful exit from a family business is more than a transaction. It is a handoff of hand-built purpose, values, and legacy. Whether you’re preparing to retire, developing the next generation of leaders, or considering a potential sale, an early start and a trusted advisory team can meaningfully improve outcomes.

Working alongside a financial professional can help you evaluate valuation, tax, and liquidity decisions while keeping family dynamics steady. With coordinated planning, you can build a transition that protects what you’ve created and supports the people who rely on it.

Ready to Get Started?

Schedule a consultation to discuss your timeline, goals, and next steps for family business and succession planning. We’ll help you plan your next steps forward with confidence.

For a comprehensive review of your personal situation, always consult with a tax or legal advisor. Neither Cetera Wealth Services, LLC nor any of its representatives may give legal or tax advice.