Why It Matters and How to Put It Into Practice

Retirement changes the shape of healthcare. You may have more flexibility in your schedule, but you are often working with steadier income and less tolerance for surprise costs. Medical self-advocacy is how you keep care decisions aligned with the life you want to live and the plan you have built.

At its best, self-advocacy is calm, clear, and practical. It helps you get better answers, follow through at home, and reduce the odds that a medical decision creates unnecessary financial friction later.

Defining Medical Self-Advocacy

Medical self-advocacy is the practice of matching healthcare decisions to the life you’re trying to live, including the logistics, the costs, and what you can realistically manage at home. It starts with clarity about what matters most right now: independence, pain control, longevity, time at home, energy for grandchildren, or a specific blend in a specific order. When clinicians have that context, visits usually become more productive and recommendations are easier to evaluate.

It is also relational. Clinicians do their best work with a partner who shares goals, asks for plain language, and speaks up when a plan will be hard to execute at home. You do not need medical training. You need the willingness to name the goal, ask for the tradeoffs, and leave with a next step you can actually follow.

Key Takeaways

In retirement, medical self-advocacy is about getting care that fits your priorities and your real-life constraints, including budget, support at home, and lifestyle goals. It also reduces the chance that a small administrative issue becomes an expensive surprise.

Start visits with a clear outcome you care about, then ask direct questions and write down the plan before you leave.

Put decision-making in writing with a medical power of attorney and an advance directive so your care team and family can act quickly when timing matters.

Ask early about site of care, second opinions, and medication alternatives since these choices often shape out-of-pocket costs as much as the treatment itself.

Medicare coverage rules, prior authorizations, and appeals are manageable when you keep the denial, dates, names, and a short log of calls in one place.

Coordinate major care decisions with tax timing, monthly cash needs, and long-term care planning to keep flexibility across a long retirement.

Together, these steps help you stay engaged in decisions, reduce stress for loved ones, and keep your broader retirement plan on track.

Why Retirement Raises the Stakes

In retirement, time looks different. There may be more time for appointments and recoveries, yet income is usually more fixed. Healthcare needs can increase, and even small administrative missteps can echo through a monthly budget. A missed referral, an out-of-network facility, or a specialty drug that lands on a higher formulary tier can create surprise costs that feel avoidable in hindsight.

The communication side matters just as much. Adult children may live far away. A spouse may be a great caregiver but uncomfortable pressing for details. Clear self-advocacy gives everyone a shared script. It turns vague stress into specific tasks like confirming a facility is in network before scheduling, or asking whether home-health qualifies given your situation.

What to Do Before, During, and After Appointments

A simple way to advocate for yourself is to begin each appointment with a goal, not a symptom list. Tell your clinician what matters most and how you define success. For example: “My goal is to stay at home safely and keep walking the dog, so I want knee options that keep recovery manageable.”

That one sentence anchors the conversation around your priorities. From there, keep the discussion focused with three types of questions. Options: What approaches best support the goal you just stated? Outcomes: What benefits and side effects are most likely for someone your age and health profile? Setting and cost: Can any of the work be done at a lower-cost site without sacrificing quality?

Before you leave, make sure you have a written plan. If an after-visit summary is not automatically provided, ask for one. If your condition shifts at home, you will have a shared reference for what to try first and who to call. That small step often reduces confusion, extra copays, and the stress that comes from guessing.

When Health Decisions Become Money Decisions

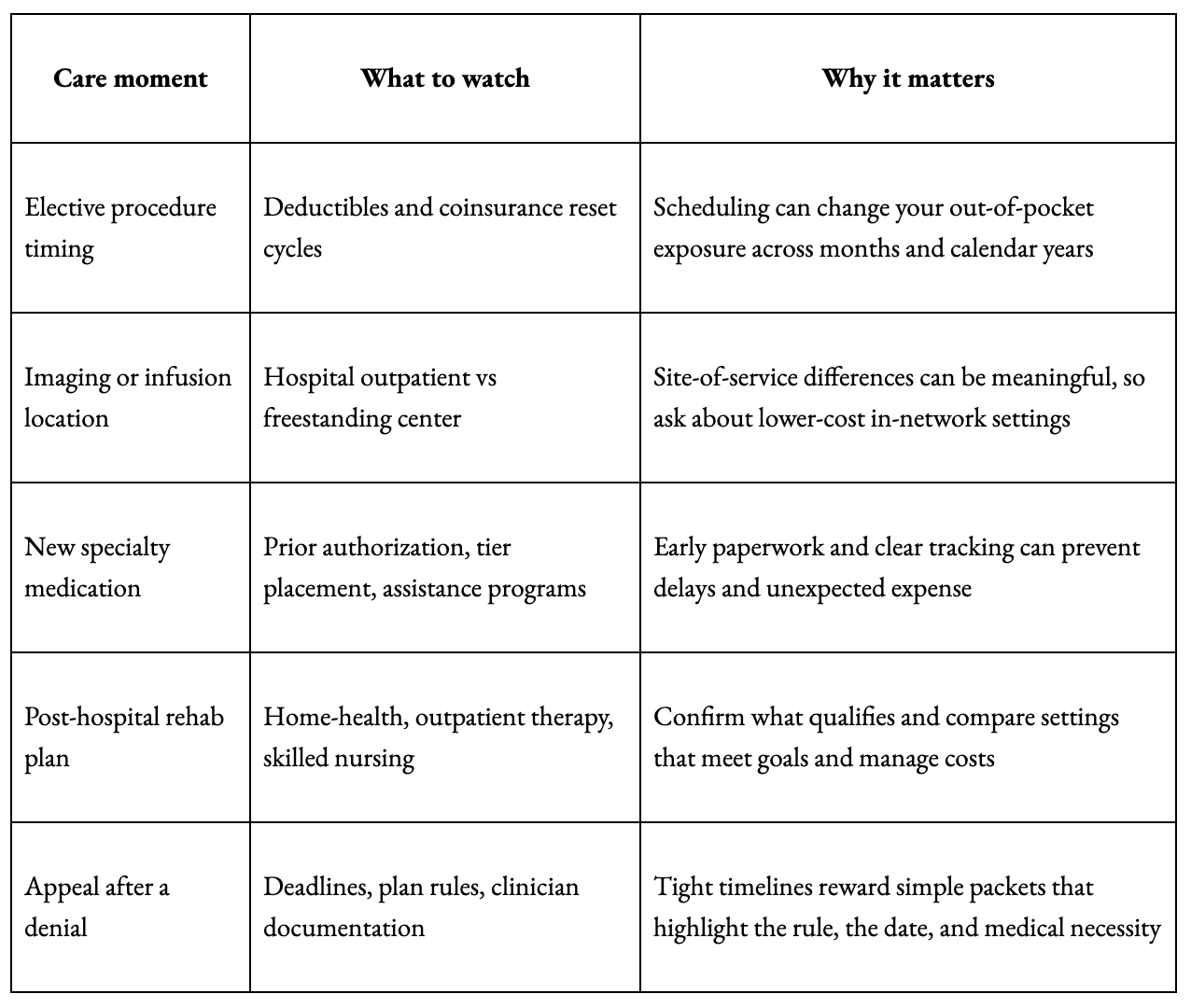

Linking clinical choices with financial realities should feel natural, not forced. The most obvious connection is where and when care happens. A hospital outpatient department can bill differently than a freestanding center. The same imaging study or infusion can come with very different out-of-pocket exposure depending on the site of service and the way it is coded. Asking about setting is not second-guessing care. It is a practical part of planning.

Medications tell a similar story. A periodic review can uncover duplications, interactions, or therapeutically similar options on a lower formulary tier. In some situations, 90-day fills and preferred mail-order pharmacies reduce recurring costs and make it easier to stay consistent. These are practical moves that support both health and household budgets.

Below is a compact snapshot of common care moments in retirement and how they tend to connect to finances. Think of it as a quick crosswalk for reducing surprises, not a checklist you have to follow perfectly.

Proactive self-advocacy often prevents hurried, more expensive defaults. The point is not to avoid care. The point is to plan care strategically, including setting, timing, and documentation, so health can improve while your monthly budget stays steadier.

Next, make sure your preferences and decision-making structure can travel with you through the system, especially when timing is not on your side.

If you want to coordinate how healthcare decisions may affect taxes, cash flow, Medicare premiums, or long-term planning, contact the office at Archstone Financial to schedule a consultation.

The Two Documents That Reduce Family Stress

Two documents consistently lower friction for families and clinicians, especially when a spouse or adult child needs to step in quickly:

A medical power of attorney names a person you trust to speak for you if you cannot. An advance directive guides that person and your care team on preferences such as CPR, ventilation, feeding tubes, and comfort measures.

Bring copies to admissions, upload them to major patient portals, and make sure your decision-maker knows where the originals are stored at home. This is not paperwork for its own sake. It is a practical way to reduce uncertainty when decisions are time sensitive.

Integrating Advocacy With Retirement Planning

Your medical and financial choices often influence each other, especially in retirement. Connecting these areas early can reduce avoidable costs and protect flexibility when health needs or income change.

Tax timing and Medicare premiums can intersect in uncomfortable ways. A one-time spike in taxable income can increase Medicare premiums later through income-related monthly adjustment amounts (IRMAA), which is the Medicare premium surcharge tied to income. If a major procedure or a new recurring-cost medication lands in the same window, timing and planning can help prevent multiple cost pressures from stacking at once.

Health Savings Accounts can also play a role. If you still have an HSA from your working years, those funds can pay for qualified medical, dental, and vision expenses tax-free. Using HSA dollars for care preserves taxable cash for everyday needs and makes it easier to say yes to recommended care without straining the budget.

Long-term care insurance is another place where documentation matters. Many policies require clear records showing help needed with Activities of Daily Living or cognitive testing before benefits begin. Asking a clinician to chart limitations precisely can speed a claim and reduce back-and-forth.

Finally, remember that billing support exists. Nonprofit hospitals publish financial assistance policies that may include discounts or interest-free payment plans. Asking about options before an elective procedure gives you time to plan in a calmer moment.

Bringing financial awareness into medical conversations is not overstepping. It is a way to protect flexibility when health costs and retirement income have to coexist.

Navigating Medical Bills Without Guesswork

Even with good planning, medical bills can be confusing. Self-advocacy continues after the visit by making sure statements are accurate and you understand what you are paying for.

Compare the explanation of benefits (EOB) to the provider bill to spot discrepancies.

Request an itemized bill so you can verify charges and catch duplicates or coding errors.

Confirm network status and coding details when something looks off, since errors can often be corrected before payment.

Ask about interest-free payment plans, which are common even for insured patients.

If the balance is large, ask whether prompt-pay discounts or financial assistance programs apply, and keep a record of who you spoke with and when.

These habits help prevent overpayment, protect cash flow, and reduce stress for you and your family.

Keeping Self-Advocacy Sustainable

Most people do not want their own healthcare management to turn into an ongoing administrative job. A few light-lift habits keep the effort small and the payoff meaningful.

Start with a one-page health snapshot: diagnoses, surgeries, allergies, medications with doses, decision-makers, and insurance details. Keep it current, upload it to portals, and carry a paper copy. Before each visit, choose one priority question and two backups. If someone helps you day-to-day, invite them to join by phone so the plan is heard the same way by everyone.

Then pace decisions to the stakes. Reversible, low-risk choices can move quickly. High-stakes or irreversible choices often deserve a night to think, a second opinion, or a call to confirm network status. Deliberate does not mean slow. It means right-sized.

Authorizations, Appeals, and the Clock

The administrative layer of healthcare can feel opaque, but it is navigable. When a service is denied or shortened, there is usually a path to request review, and deadlines are often short.

Save the denial letter and note the date. Ask the clinician for a brief letter explaining medical necessity, and include relevant notes when appropriate. If you have the plan rule or coverage policy, reference it directly. Keep a simple log of calls and portal messages so you can quickly answer the questions plan providers typically ask. This is not about building a binder. It is about keeping a small, relevant record that travels well.

Setting Up Your Support Team

Self-advocacy often becomes family advocacy after a hospital stay or during rehabilitation. If a spouse or adult child will serve as the point person, set them up to succeed.

Make sure they have access to your medical power of attorney and a HIPAA release so they can speak directly with offices and providers. Keep medication lists, clinician contacts, and insurance IDs in one place. Also agree on how updates will be shared with other relatives so the caregiver is not managing a swirl of texts when rest is needed most.

When your helpers know what to do and have permission to do it, they can focus on presence rather than paperwork.

Frequently Asked Questions About Medical Self-Advocacy

The questions below reflect common retirement-planning concerns that blend healthcare decisions, Medicare rules, and household finances.

How can retirees reduce Medicare premiums, including IRMAA?

IRMAA (Income-Related Monthly Adjustment Amount) is the Medicare premium surcharge tied to income, and it is based on prior-year tax information. If you are anticipating a one-time income spike, it can help to coordinate the timing of tax events and major healthcare expenses so you are not hit with higher premiums and higher out-of-pocket costs in the same stretch. In practice, this often starts with forecasting taxable income and watching the timing of withdrawals or large transactions.

What should I ask to avoid surprise out-of-pocket costs for procedures, imaging, or infusions?

Start by asking whether the service can be done at an in-network, lower-cost site without sacrificing quality. Hospital outpatient departments often bill differently than freestanding centers, even within the same system. Pair that question with a request to confirm network status before you schedule, and write down the name of the person who verified it.

What can I do if my Medicare Advantage plan denies a service my clinician recommends?

Move quickly and keep it simple. Save the denial letter, note the date, and ask your clinician for a short medical-necessity statement that directly addresses the reason given for the denial. When available, reference the plan rule or coverage policy. Medicare Advantage appeals typically start with a reconsideration request to the plan, and tight deadlines are common.

How can I lower prescription drug costs on Medicare without changing outcomes?

Ask about therapeutic equivalents on lower formulary tiers, preferred pharmacies, and 90-day fills when appropriate. If a drug is not covered or is placed on a higher tier, your clinician may be able to support an exception request when medical necessity is documented. Keep approvals, denials, and prior authorization steps in writing so you can track what is still pending.

What legal and planning documents should retirees have for medical decisions?

A medical power of attorney names who can speak for you if you cannot, and an advance directive documents your care preferences. Bringing copies to admissions, uploading them to portals, and telling your decision-maker where originals are stored can prevent delays and reduce stress when decisions are time sensitive.

Advocacy That Protects Your Retirement Plan

Medical self-advocacy in retirement comes down to a few repeatable moves:

Start appointments with a clear goal.

Ask for plain-language options and tradeoffs

Leave with a written plan you can follow at home.

Support those conversations with clear, organized documentation, including a medical power of attorney and an advance directive, so your wishes are clear if decisions become urgent.

From a planning standpoint, self-advocacy also means paying attention to the cost drivers that tend to surprise retirees, including site-of-service pricing, formulary tiers, prior authorizations, appeal deadlines, and the way major care decisions can intersect with taxes and Medicare premiums. When you keep simple records and coordinate medical choices with household cash flow and long-term planning, you reduce avoidable friction and preserve flexibility.

If you have questions regarding medical self-advocacy, financial planning, insurance, or other related questions, contact the office today to schedule a consultation. Together, we can map out your next steps and develop a coordinated plan.