Retirement often gives you the space to think beyond schedules and portfolios. With a little more time and perspective, many people start asking what they want to stand for, and what they want to leave behind. Legacy and estate planning in retirement is a big part of that, but it is not only about documents. It is about shaping how your values, generosity, and life lessons keep influencing others, both now and in the years ahead.

That idea is captured in a living legacy. It brings together what you believe, how you live, and how you steward the resources you have built for the people and causes you care about. The choices you make today can reduce future burdens, make your intentions more understandable, and help your story continue in a way that feels true to you.

In this guide, you’ll explore how to:

- Define what a “living legacy” really means, and why it matters.

- Connect personal values to the structure of your estate and giving plan.

- Use tax-efficient tools like required minimum distributions (RMDs), qualified charitable distributions (QCDs), and donor-advised funds (DAFs).

- Start meaningful family conversations that reduce confusion later.

- Keep your plans current through simple annual reviews.

Together, these steps can help you shape a legacy that is lived today and prepared for tomorrow. Let’s start by clarifying what “living legacy” really means, and how it fits within a broader legacy and estate planning strategy.

A Living Legacy Is More Than Paperwork

Legacy is often described as paperwork, such as a will, a trust, or beneficiary forms. Those pieces are crucial, but they do not tell the whole story. A living legacy also shows up in the mentoring call that becomes a monthly habit, the volunteer work that gives your week purpose, or the steady support that helps a local program stay strong.

A living legacy is your character in motion. It is also practical in ways people sometimes overlook. Clear medical preferences, coordinated beneficiary designations, and a plan for who handles what if something happens can be just as meaningful as any financial gift.

This perspective matters even more because many retirements now last a long time. Recent longevity data shows that many retirees are planning for decades of purpose, not a short final chapter. That longer horizon gives you more opportunity to live your values in the present while shaping what endures later.

Turning Intentions Into A Clear Structure

Strong plans begin in plain language. Take a few minutes to write down the values you want to keep traveling forward, such as generosity, stewardship, curiosity, faith, care for family, or care for the natural world. Then list the people or causes you most want those values to reach.

If you can, add one or two short stories that explain why those values matter to you. That narrative will guide decisions more clearly than a spreadsheet alone. Once you have that foundation, you can layer in the structural tools that help those intentions carry forward.

- Required minimum distributions (RMDs) are one key example. For most retirees, tax deferred accounts require minimum annual withdrawals starting at age 73. Coordinating those withdrawals with family support or charitable giving can turn a compliance requirement into a legacy habit that fits your values. Read further about RMDs.

- Qualified charitable distributions (QCDs) can also support that approach. If you are 70½ or older, you can direct a QCD from your IRA to an eligible charity. When handled correctly, it is excluded from taxable income and can satisfy all or part of that year’s RMD. The annual cap is inflation indexed, and current limits are updated regularly. Learn more about QCDs.

- Donor-advised funds (DAFs) are another flexible tool. With a DAF, you make a charitable contribution, take an immediate deduction within IRS limits, and recommend grants over time. Many retirees like DAFs because they simplify giving and recordkeeping while letting generosity unfold gradually. Get more information about DAFs.

- Finally, charitable remainder trusts (CRTs) may be a fit for some families. These irrevocable trusts can provide income during your lifetime and direct remaining assets to charity afterward. They are often useful for retirees with highly appreciated assets who want a balance of lifetime income and long range giving. Learn more about CRTs.

The right combination depends on your goals, your tax picture, and what feels manageable over time.

Family Conversations That Ensure Your Plan Works

A plan that is not shared is a plan that can unravel. The people who might one day carry out your wishes need to understand what you want, why you want it, and how to follow through. One clear conversation can create more alignment than a stack of forms.

Two topics are usually worth tackling early.

- First, medical preferences. Advance care planning involves choosing a health care proxy, documenting your wishes, and making sure loved ones know what you want. These steps reduce uncertainty when decisions are hardest.

- Second, survivor benefits. If a spouse, child, or dependent parent may rely on survivor income, make sure they know what is available and how to begin drawing benefits when the time comes. Clear expectations now can spare loved ones from scrambling later.

Legacy and estate planning topics can feel heavy. Many families find it easier to engage when they are framed as acts of care that protect dignity and reduce future stress.

How To Live Your Legacy Right Now

A living legacy does not require grand gestures. More often, it grows through ordinary rhythms and repeated choices. It shows up in who gets your time, what you support, and which habits become part of your family’s culture.

- For example, presence can be a legacy practice. A regular coffee with a younger neighbor or relative, paired with listening and encouragement, is often remembered for years.

- Generosity can also take a simple, repeatable form, such as tying giving to your RMD timing, your birthday month, or a shared family passion like parks, literacy, or food security.

- Storytelling is another quiet but powerful legacy habit. Short voice memos about lessons learned, favorite memories, or turning points, along with photos labeled with real context, help your values stay vivid for the next generation.

None of these require large sums of time or money. Yet they shape how people understand what mattered to you, and how they might carry it forward.

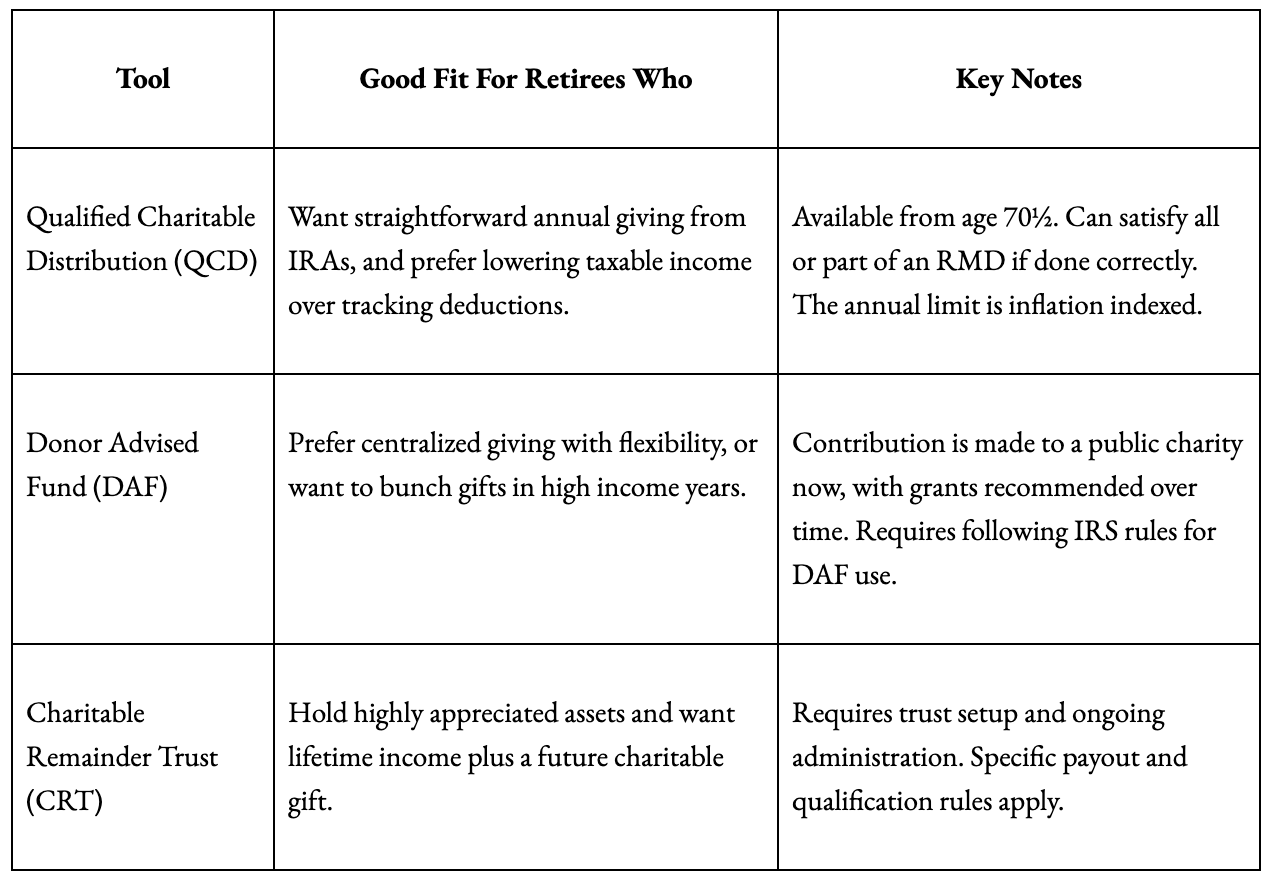

Common Giving Tools At-A-Glance

The table below highlights three frequently used charitable tools. It does not replace personalized advice, but it can help you explore options to discuss with your financial professional.

Choosing a structure that matches your intent can make giving easier to sustain during life and more likely to continue afterward.

A Simple Yearly Review That Prevents Drift

Even well built plans drift if life changes and documents do not. A yearly check, plus updates after major events, keeps your living legacy aligned with your real situation.

Start by confirming beneficiaries and titling. Beneficiary designations on retirement accounts and insurance policies usually override wills and trusts, so it is worth making sure they still reflect your intent. Next, keep giving consistent by setting reminders for QCDs or DAF grants, especially if generosity is a core value in your plan. Finally, revisit medical documents periodically. After major family changes, check that your health care proxy and directives still match your wishes, and be sure trusted people know where those documents are stored.

This routine maintenance is simple, but it can help prevent a lot of confusion later.

Addressing Unique Family Needs Head-On

Blended families, special needs dependents, family businesses, or shared property can add layers to legacy and estate planning. The key is not waiting for everything to feel simple. Instead, address complexity directly, with clarity and care.

It often helps to:

- Explain in writing why gifts or provisions are structured the way they are.; that context can reduce misunderstanding later.

- Clarify roles, such as executor, trustee, power of attorney, and health care proxy, and to name alternates.

- Keep documents, contacts, and account instructions in one organized place so loved ones are not searching during a difficult moment.

- Make sure your family understands how survivor benefits work and where to begin (if applicable to your situation).

These steps will not remove every question, but they can reduce uncertainty and conflict in a meaningful way.

Frequently Asked Questions About Living Legacies And Legacy Planning

Even with a clear plan, a few practical questions tend to come up as people begin thinking through what a living legacy looks like in real life. The answers below are meant to offer steady footing and help you identify topics worth discussing with a financial professional.

What’s The Difference Between A Living Legacy And Traditional Estate Planning?

A living legacy is the day to day expression of values through mentoring, volunteering, generosity, and communication with loved ones. Estate planning supplies the documents and designations that keep those values moving after you are gone. Both matter. Beneficiary forms on retirement accounts often control who receives those assets, even if a will says something different, so keeping designations aligned with your intentions is essential.

How Do Required Minimum Distributions Fit Into A Living Legacy?

RMDs are mandatory withdrawals from most tax deferred retirement accounts starting at age 73 for many retirees. Coordinating an RMD with gifts to family or charity can turn a rule based withdrawal into a meaningful legacy routine. It is a way to let your values guide a financial step you already have to take.

I Already Give To Charity. What’s The Simplest Way To Align That With Retirement Tax Rules?

If you are 70½ or older and give regularly, a QCD may be a simple fit. It is a direct IRA to charity transfer that can be excluded from taxable income when executed correctly, and it can count toward that year’s RMD. For many retirees, it is one of the cleanest ways to connect generosity with tax planning.

What Conversations Can Reduce Confusion For My Family Later?

Two conversations usually help most. One is advance care planning, which covers who is your health care proxy, what your medical preferences are, and where documents are kept. The other is survivor benefits, especially if a spouse or dependents may rely on Social Security after your death.

How Often Should I Review Beneficiaries, Titling, And Documents?

A quick review once a year, and another after major life events, is a practical approach. Confirm that beneficiary designations match your intent, account titling supports the plan, and medical directives still reflect your wishes. Regular small updates prevent large surprises later.

Is There A Way To Keep Giving Consistent Without Feeling Overloaded By Administration?

Yes. Many retirees tie giving to simple calendar cues, like an RMD month or a birthday month. A DAF can reduce recordkeeping and help you pace grants over time, while QCDs can keep giving steady and reduce taxable income when used correctly.

What’s An Underrated Element Of A Living Legacy?

The story behind the plan. A brief values letter or ethical will gives meaning to the numbers and helps loved ones understand your intent. When that narrative is paired with accurate beneficiary forms, clear medical directives, and the right charitable tools, your legacy becomes easier for others to carry forward.

Closing Thoughts On What Endures

A living legacy is not reserved for the end of life. It is built through everyday choices, steady practices, and clear communication. How you spend time, how you show generosity, and how you explain your decisions all shape what endures.

The technical pieces like RMD timing, QCD limits, DAF rules, CRT administration, medical directives, and survivor benefits are there to support that bigger vision. Underneath it all is something simpler: the values you want to last, and the people and causes you trust to carry them forward.

If you want to explore how these ideas connect to your own legacy and estate planning goals, reach out to the office to schedule a conversation with your financial professional. Together, we can build a plan that reflects your life today and supports the impact you want to leave behind.