Many people think of legacy as the money they’ll leave behind. But inheritance is just the starting point. A true legacy goes deeper—it’s the principles, priorities, and plans that turn wealth into a lasting guide for future generations.

A meaningful legacy offers more than financial assets; it provides clarity during uncertainty and stability when big decisions arise.

A lasting legacy connects purpose to structure. It clarifies who’s included, how assets support life goals, and what practices can help keep decisions aligned—through both calm and volatile markets.

This guide outlines specific steps you can take now to build a legacy that lasts. Use it to start family discussions, define priorities, and coordinate your team of professionals so your plan stays adaptable as circumstances, tax laws, and markets evolve.

Reframing Wealth: Beyond Balances to Family Results

Reaching certain goals for your wealth is important, but this doesn’t guarantee your legacy will endure. Without intention, wealth can easily erode through taxes, fees, or rushed decisions made under stress.

Begin by defining what a lasting legacy means for your family:

- Who benefits?

- Which needs are essential?

- How much discretion should heirs have?

- How will conflicts be resolved?

One helpful strategy is to capture these decisions on a single page and revisit them each year to make updates as needed.

When money supports clearly defined outcomes, inheritance evolves into stewardship—and stewardship becomes the foundation of an enduring legacy. If it might be helpful, ask your financial professional to facilitate a short goals session and document the results for easy reference later.

Four Pillars For Building an Enduring Legacy

Here are four key building blocks that can help turn legacy planning from concept to reality:

- Governance: Create a simple family mission statement, decide how often you’ll meet, and clarify who makes which decisions.

- Structures: Align account titling, beneficiary designations, and trust documents with your goals and protections.

- Financial Engines: Define cash-flow sources, rebalancing rules, and reserves for unexpected needs.

- Human Capital: Equip future generations with skills, mentoring, and accountability, not just distributions.

Start with a working draft and refine it over time. A brief consultation with a financial professional can reveal where your accounts, documents, and intentions may be out of sync—and help prioritize updates without unnecessary complexity.

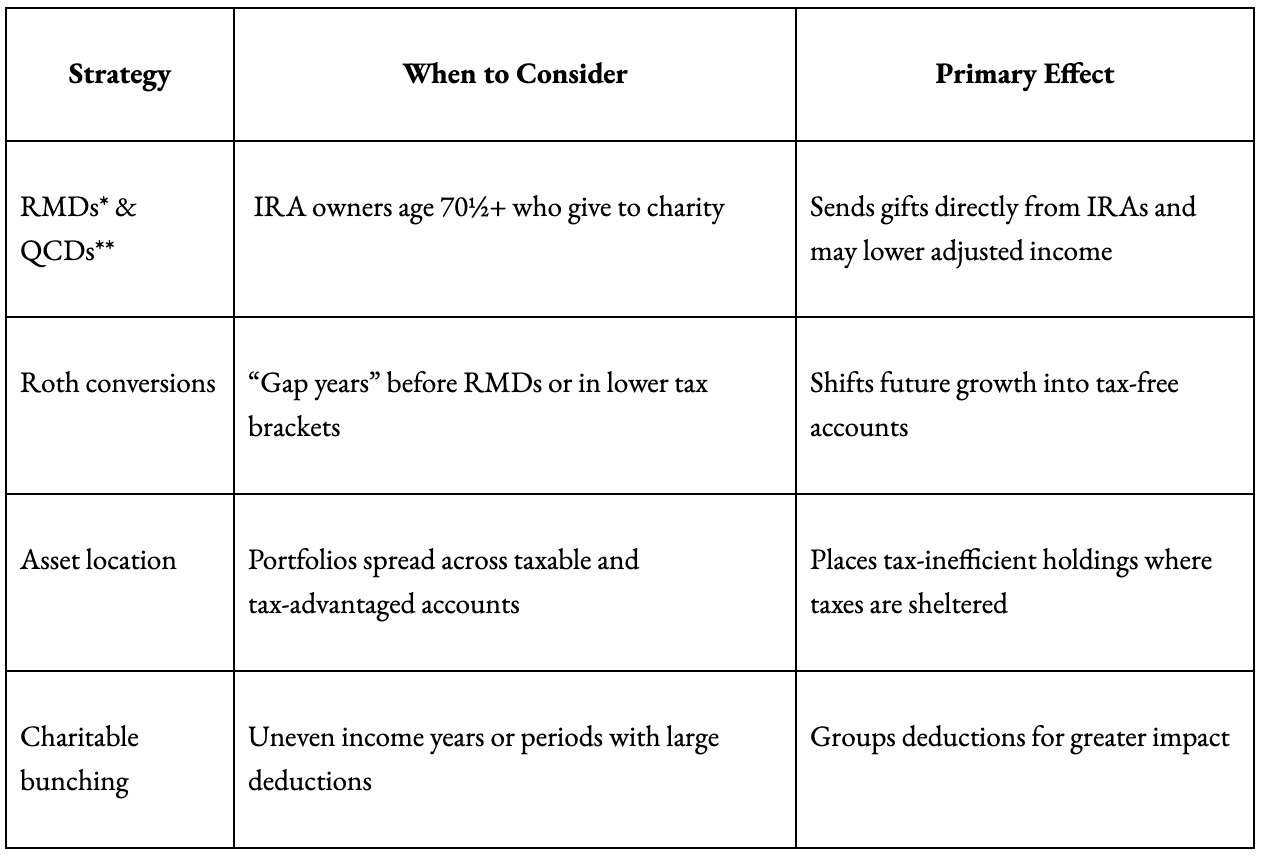

Preserving Optionality with Tax-Efficient Cash Flow

Tax-aware cash flow helps preserve choice, which is the real currency of an enduring legacy. Focus on withdrawal sequencing, charitable and advanced tax approaches, and which assets sit in which account types.

Coordinating these decisions can extend the reach of your legacy while still funding today’s lifestyle responsibly. Modeling different strategies can also show how each choice affects lifetime taxes and flexibility.

To put this into motion, request a retirement income review that maps out your withdrawal order, tax brackets, and charitable giving strategies. A one-page summary can help your plan clear and easy to revisit.

Using Trusts and Entities to Support Your Legacy

Used thoughtfully, certain legal structures can help protect your family and communicate your intent, which which are key ingredients in a lasting legacy. Common tools include revocable trusts, dynasty trusts, Spousal Lifetime Access Trusts (SLATs) that allow indirect access for a spouse, Irrevocable Life Insurance Trusts (ILITs) for estate liquidity, and charitable vehicles such as donor-advised funds or charitable remainder trusts.

Design choices matter because they can significantly impact outcomes. Trustee authority, distribution rules, and education for beneficiaries all influence how effectively your legacy carries forward.

Consider a joint advisor-attorney design session. Test your plan against real-world scenarios, like second marriages, special-needs planning, concentrated assets), so the structure stays flexible while honoring your goals. A short design audit today often prevents costly rework later.

If your documents are more than five years old or predate major law changes, schedule a focused review with your financial professional to ensure they still reflect your wishes.

Family Governance: Sharing Wisdom Alongside Wealth

Strong governance can help keep a legacy from functioning like a blank check. Start by writing a one-page family mission statement and set a regular meeting schedule—perhaps quarterly for adults, with an annual full-family meeting.

Use agendas that connect investing, giving, and learning back to your priorities and shared values. Consider writing letters of wishes to provide additional context for trustees and heirs. Gradually increasing transparency helps younger generations gain confidence and practice stewardship before taking on more responsibility.

If desired, your financial professional can help you establish family governance guidelines, facilitate family meetings, and document roles, agendas, and follow-ups.

Investment Policies for Multi-Generational Wealth

A portfolio that’s designed to serve multiple generations will often benefit from a written policy that ties purpose, risk, and spending to your legacy.

Favoring a total-return approach (rather than focusing solely on yield) can help align investments with long-term objectives. Setting clear risk parameters may also make it easier to stay the course when markets fluctuate. Many families choose to maintain a liquidity sleeve for near-term needs and follow structured rebalancing guidelines to keep decisions consistent over time.

A broadly diversified portfolio, combined with thoughtful inflation awareness, can help support stability and continuity across generations. Ask your financial professional to review your Investment Policy Statement to ensure it aligns with your time horizon and family governance plan.

Preparing Heirs with Skills, Access, and Accountability

Preparation beats surprise. An enduring legacy helps develop people as intentionally as it grows portfolios.

Consider starting with some low-stakes exercisess: pay a batch of bills, review statements together, or make a modest grant using your agreed rubric. Offer mentoring, gradually involve adult children in financial meetings, and offer age-appropriate challenges to younger children. Incentive provisions can reward effort without burying the legacy under conditions or creating dependency.

Ask your financial professional about age-appropriate education resources and a roadmap for increasing responsibility over time. Independent financial guidance for heirs can also minimize family friction and build confidence.

Simplifying Real Estate Transfer and Business Succession

Real estate and closely held businesses can help anchor a legacy, but they can also add complexity. Confirm titling, beneficiary deeds where available, and treatment of mortgages or credit lines. Keep a property “playbook” that lists contacts, leases, insurance, basis, and maintenance schedules.

For businesses, a buy-sell agreement funded with insurance, if appropriate, can help safeguard the legacy if a partner exits, retires, or dies. Review valuation methods, key-person coverage, and successor training regularly.

Your financial professional can coordinate with your CPA and attorney to ensure tax elections and operational practices work together seamlessly.

Supporting Stewardship and Tax Strategy Through Philanthropy

Philanthropy often serves as both a value and a strategy. It can teach the next generation to give with intention and can help reduce tax exposure—two benefits that can strengthen a legacy.

Begin with structure. Select a donor-advised fund or a private foundation, and consider moves such as charitable bunching or donating appreciated positions to enhance impact.

Make giving participatory and collaborative. Involve younger family members in vetting charities, setting grant targets, and tracking outcomes. A simple quarterly giving meeting can help ensure generosity remains organized and aligned with your values.

A financial professional can help design your giving framework and annual calendar so charitable action becomes a consistent part of your family’s legacy.

Legacy Planning Documents: A Practical Checklist

Use this checklist to help convert your goals and intentions into a clear plan that supports your legacy.

- Up-to-date will, revocable trust, powers of attorney, and health directives

- Confirmed beneficiary designations, including contingent and per-stirpes

- Comprehensive asset inventory with titling, cost basis, and key contacts

- Investment Policy Statement, rebalancing rules, liquidity sleeve, and spending rate

- Trustee guidance or letter of wishes with distribution approach

- Philanthropy plan with grant rubric and calendar

- Family meeting cadence, agenda template, and assigned responsibilities

- Secure digital vault with shared access and emergency instructions

Mark any completed items, then choose one priority to address this quarter.

Frequently Asked Questions About Legacy Building

Here are some common legacy questions that often surface at the very start of legacy and estate planning processes.

What belongs on page one of a legacy plan?

Start with purpose, people, and process. Spell out the family’s aims, who participates and in what roles, and how decisions are made so the legacy plan can guide practical steps that support your wishes.

Where do taxes most affect long-term outcomes?

Timing and sequence matter. Withdrawal order, Roth conversions, and QCDs can reduce drag, helping a legacy support lifestyle and giving. Simple modeling can show how modest adjustments today may preserve flexibility over decades.

Are trusts only useful for very large estates?

Not necessarily. Revocable trusts streamline administration; dynasty trusts add protections; SLATs and ILITs address access and liquidity needs. The right tool is the one that advances your objectives without unnecessary complexity, with distribution language that teaches stewardship.

How can generosity be encouraged without fostering dependency?

Education, phased transparency, and incentives can help. Consider tying distributions to milestones, learning, or service so the legacy highlights contribution and preserves personal agency.

What keeps multi-generation investing disciplined?

A written policy that sets a spending approach, risk budgets, rebalancing bands, and a plan to replenish the liquidity sleeve. Linking these rules to a time horizon can help align near-term needs with long-term intent.

How often should the family review the plan together?

Hold family meetings at least annually, with extra check-ins around major life events. Use agendas tied to the family mission, keep minutes and next steps visible, and reinforce the legacy through consistent practice.

Next Steps for Establishing an Enduring Legacy

Legacy planning often delivers the most value when good intentions are translated into clear, coordinated steps. If you’re ready to organize or refresh your enduring legacy, your financial professional can help you prioritize actions and coordinate necessary updates with your tax and legal team.

A focused conversation can surface what is already in place, highlight gaps, and create momentum toward an integrated plan—one that not only preserves wealth but also supports and strengthens the values behind it..

Contact the office to schedule a meeting, and let’s start making your legacy a living, guiding, enduring force for generations to come.

Cetera Wealth Services, LLC exclusively provides investment products and services through its representatives. Although Cetera does not provide tax or legal advice, or supervise tax, accounting or legal services, Cetera representatives may offer these services through their independent outside business. This information is not intended as tax or legal advice.

*RMD - Required minimum distribution

**QCD - Qualified charitable distribution